by Alex Polorotoff

Understanding when an SMSF requires an actuarial certificate is essential for accurate ECPI calculation and ATO compliance. This article outlines the key rules, methods, and scenarios that determine whether an actuarial certificate is needed, helping you guide your clients through complex fund structures and reporting obligations.

Whether your clients are using the segregated or proportionate method, or switching between the two during a financial year, this guide will clarify what to look out for. For experienced practitioners, we also address mixed-period strategies, the implications of reserve accounts, and how actuarial percentage calculations apply to periods of proportionate use only.

There are two methods for calculating exempt current pension income (ECPI): the segregated method and the proportionate method. The correct method depends on the SMSF’s structure and how its assets support retirement-phase income streams.

In short, an SMSF may need an actuarial certificate even when using the segregated method, especially if contributions or rollovers create accumulation balances during the year.

For a full breakdown of when each method applies, how they affect ECPI, and when a certificate is legally required, see our Actuarial Certificate service page.

SMSFs using the proportionate method will need an actuarial certificate if they wish to claim exempt current pension income (ECPI). This requirement applies not only in scenarios where both accumulation and pension balances exist, but also when reserve accounts are present in the fund.

Reserve accounts are balances held within the SMSF that have not yet been allocated to a specific member’s account. These balances will only count towards a member’s total once they have been formally credited. It is essential to keep in mind that reserve accounts can only be maintained if they comply with SIS regulations and align with the governing rules in the SMSF Trust Deed.

In practical terms, reserve accounts may arise from insurance proceeds, employer contributions, or forfeited member benefits. However, their use must be carefully managed to ensure the fund remains compliant and avoids any potential breaches of ATO guidelines.

An actuarial certificate is required under the proportionate method because the SMSF must calculate the average proportion of pension liabilities to total liabilities during the relevant period. The resulting actuarial percentage is then applied to the fund’s assessable income to determine the portion that is tax-exempt under ECPI provisions.

Additionally, net capital losses that occur during the financial year are excluded from the ECPI calculation based on the actuarial certificate. These losses are not lost, they can be carried forward and applied against future capital gains, offering long-term tax planning opportunities for SMSF clients with diversified or complex investment strategies.

Following are some SMSF ECPI calculations to assist with identifying when an actuarial certificate is required:

So, in example 4:

An actuarial certificate is required for the periods where the proportionate method was used, and that percentage will only apply to those periods. Where the segregated method applied, 100% ECPI is claimed.

It is essential to ensure the correct method is used when calculating exempt current pension income (ECPI) in an SMSF. Applying the wrong ECPI percentage or selecting the incorrect method, segregated vs. proportionate, can result in an amended assessment from the ATO, exposing your client to an unexpected SMSF tax liability.

Mistakes in ECPI reporting can also delay the finalisation of the SMSF Annual Return, create unnecessary audit complications, and risk compliance breaches.

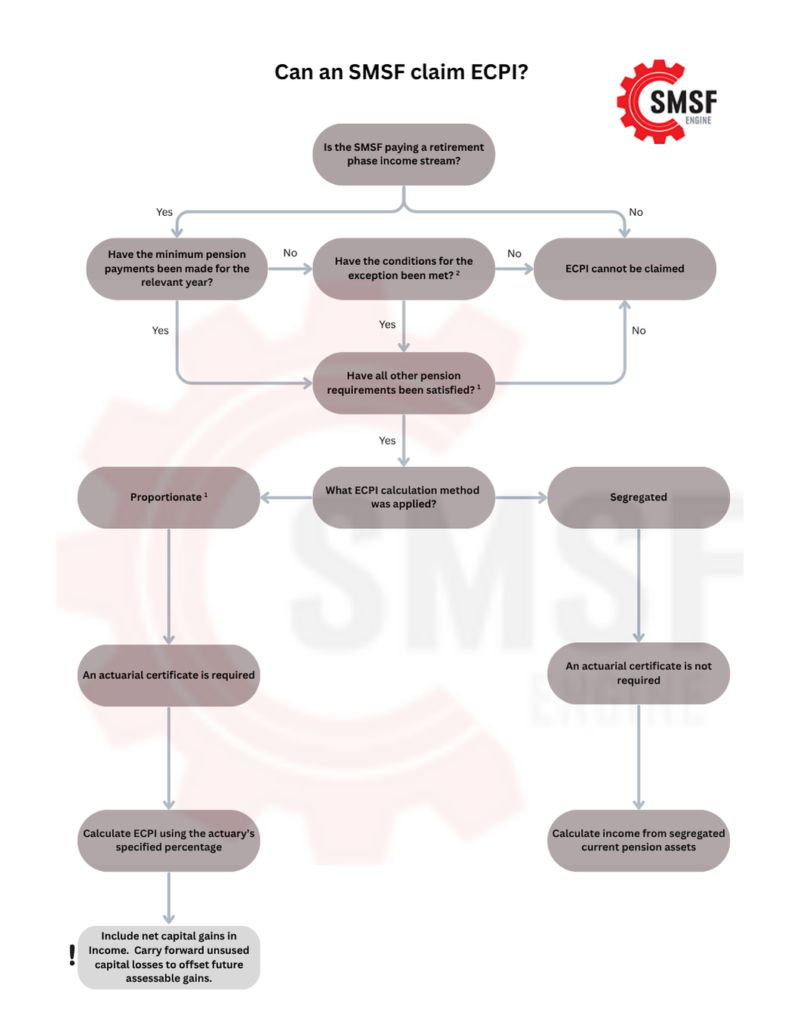

To help assess whether an SMSF is eligible to claim ECPI and determine which method applies, we’ve developed a clear and practical tool. Use our ATO ECPI Flowchart below to guide your decision-making.

For additional guidance on whether an SMSF can claim exempt current pension income (ECPI), we recommend reviewing the following ATO resources:

Prefer to keep a copy? Download the PDF version of our ATO ECPI Flowchart .

This resource supports accountants and advisers in making fast, informed decisions with confidence.

Already working through a complex case? Contact us and we’ll take care of the actuarial side so you can focus on your client relationships. Get in touch here.

Tax, Preservation and Legal Guidance for Accountants and Advisers Navigating SMSF Divorce With approximately 40% of marriages expected to end […]

Using the One-Year Work Test Exemption to Maximise SMSF Contributions After Retirement Clients approaching or entering retirement often want to […]

Keep up to date with all the latest SMSF news and updates by subscribing to SMSF Engine’s newsletter.