The list of SMSF reporting requirements from the Australian Taxation Office (ATO) is short.

It covers

We’ll highlight recent changes and common pitfalls that trustees of self-managed super funds should be aware of. SMSF trustees are advised to get professional advice about complying and avoiding mistakes.

The annual return is a combined report covering both taxation and compliance with super law and regulations. An audit precedes it.

The auditor submits a report to the trustees – and a contravention report to the ATO if required.

The audit report confirms the accuracy of the fund’s financial statements and their compliance with the fund’s investment strategy, valuation of assets, and financial position. The auditor also checks general compliance with super laws, including any relevant documentation such as the trust deed, trustees’ trustee declarations, and appropriate records of trustee meetings.

Some recent changes that affect compliance should be noted:

In the past, SMSF advisers could self-assess financial reporting requirements and prepare special purpose financial statements (SPFS). Under a new Australian Accounting Standard (AASB 2020-2), financial statements must be reported according to the General Purpose Financial Statements (GPFS) standard.

Some trust deeds say financial statements will be prepared in terms of super regulations. This gives trustees some flexibility in reporting formats. If the trust deed refers more specifically to accounting standards or Australian Accounting Standards, the fund must comply with the GPFS standard.

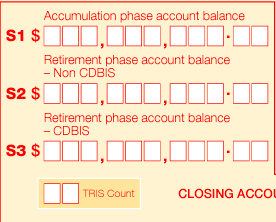

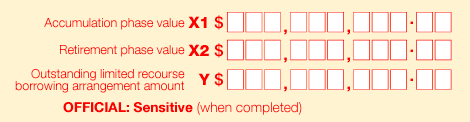

Section F of the annual return contains information about each fund member. Trustees must report specific details about member account balances, including all sources of contributions into the fund.

According to recently added requirements, trustees must report the following:

Trustees must add TRIS amounts to the accumulation account. They form part of the retirement phase only

SMSF reporting requirements changed when the ATO introduced a Transfer Balance Cap (TBC) and created Transfer Balance Accounts (TBA) for all superannuation fund members when they move from accumulation into the retirement or pension phase.

Superannuation funds have to report additional information about members in their annual return. They must also report regularly if there is an “event” related to transferring balances – i.e., the amount held in a retirement phase account.

The TBC limits the amount a member can transfer into a tax-free retirement phase account.

If a member has more than one pension fund or account, they are all added together to determine the total towards the cap.

The transfer balance cap was previously $1.6 million and increased to $1.7 million from 1st July 2021.

Individuals can see their personal TBC on the ATO online system (accessed via MyGov).

We should note that the SMSF Association believes that personal TBCs and the indexation method used to calculate them complicates an already complex area and is likely to lead to errors and breaches of limits.

It has been submitted to the government to either simplify or remove this provision. It has also asked that financial advisers be given online access to their clients’ information if they have been granted permission.

Trustees may need professional advice to ensure that they remain within the limits.

The ATO maintains a TBA on behalf of all taxpayers who have commenced a pension. The starting balance was as of 30 June 2017 for already existing pensions. Retirement phase pensions commenced after that date are added to the account balance, while any commutations reduce the balance.

The TBA is a record of transfers in and out of super accounts in the retirement phase. These transfers are called credit or debit events. The ATO uses the account to correctly maintain the member’s total super balance and to apply the provisions for transfer balance caps.

Although SMSFs report member balances in the annual return, the ATO does not use this to update TBAs.

Instead, updates are based on reports from both the SMSF and individual members. They are responsible for informing the ATO of any credit or debit event relating to the member’s pension balance.

The SMSF report is called the transfer balance account report (TBAR). The member report is called the transfer balance event notification (TBEN).

The SMSF must submit a TBAR for the following events:

Certain events affect the value of the member’s account maintained by the SMSF but do not affect the TBA held by the ATO. The SMSF does not have to report them.

These events include:

Members must report:

The ATO issues activity statements so that businesses can pay several tax liabilities simultaneously, on one form.

Business Activity Statements (BAS) apply to funds registered for GST. They are lodged either quarterly or annually.

Funds will use BAS to report on

Installment Activity Statements (IAS) apply to funds that are not registered for GST but must pay quarterly PAYG installments or PAYG withholding.

Completing these statements requires very detailed recordkeeping and the application of the correct accounting formulas.

The ATO website provides details of due dates for reporting:

However, SMSF reporting timetables depend to some extent on individual circumstances.

For example, the due dates for the annual return are generally October, February, and May. The date varies depending on whether this is the first year of your fund’s operation and whether a trustee or a tax agent is lodging the return.

For event-based reporting,

An SMSF cannot be sure of a member’s total super balance. Funds may be spread across multiple superannuation providers. A complete valuation of assets may not be possible at the start of retirement. Trustees may not know values until the SMSF’s audit has been completed.

Trustees may have to self-assess whether annual or quarterly reporting will apply.

Once this frequency has been established, this becomes the timetable for the SMSF, regardless of future member super balances.

Some special events should be reported separately or sooner.

This is usually to ensure that information from different sources can be correlated by the ATO and prevent double-counting or unnecessary commutation authorities from the ATO.

For example,

Even if an SMSF only reports annually, trustees must closely monitor events during the year to ensure that members do not exceed their caps. They may choose to report these events during the year to ensure that member TBAs are updated.

SMSF reporting requirements have been extended and have become more complex.

The ATO’s introduction of transfer balance caps and personal transfer balance accounts means that SMSFs and their members must strictly monitor and report all transactions or “events” in retirement phase accounts.

Trustees, SMSF accountants, and financial advisers with multiple SMSF clients may want to consider using expert SMSF administration services to assist them with this task.

SMSF Engine combines many years of SMSF expertise with sophisticated, cloud-based technologies. We keep member balances updated daily, identify potential compliance breaches in time, submit TBAR and BAS reports as they become due, and ensure that annual returns are submitted with minimum difficulty.

Please contact Mark Phillips or Alex Polorotoff to find out how we can help you.

One in three marriages end in divorce. For this reason, understanding some of the complexities in superannuation and tax law […]

Alex clarifies when to use an Actuarial Certificate and when you aren’t expected to.

Keep up to date with all the latest SMSF news and updates by subscribing to SMSF Engine’s newsletter.